British pensioners have far less disposable income than many of their European counterparts, figures show, increasing the likelihood that more people will need to work for longer to remain financially secure in retirement.

With the April State Pension increase approaching, new international comparisons suggest the UK continues to lag behind much of Western Europe once living costs are taken into account.

The data indicate that while the State Pension covers basic essentials for most retirees, it leaves limited room for financial resilience. As living costs remain elevated, the gap between the UK and comparable European economies is sharpening concerns about whether state provision alone is sufficient to support later life without continued earnings from work or occupational pensions.

This pressure is feeding into wider debates about retirement age, the future of the triple lock and the growing role employers play in supporting older workers who either choose, or feel compelled, to stay in work beyond traditional retirement milestones.

International comparisons highlight UK shortfall

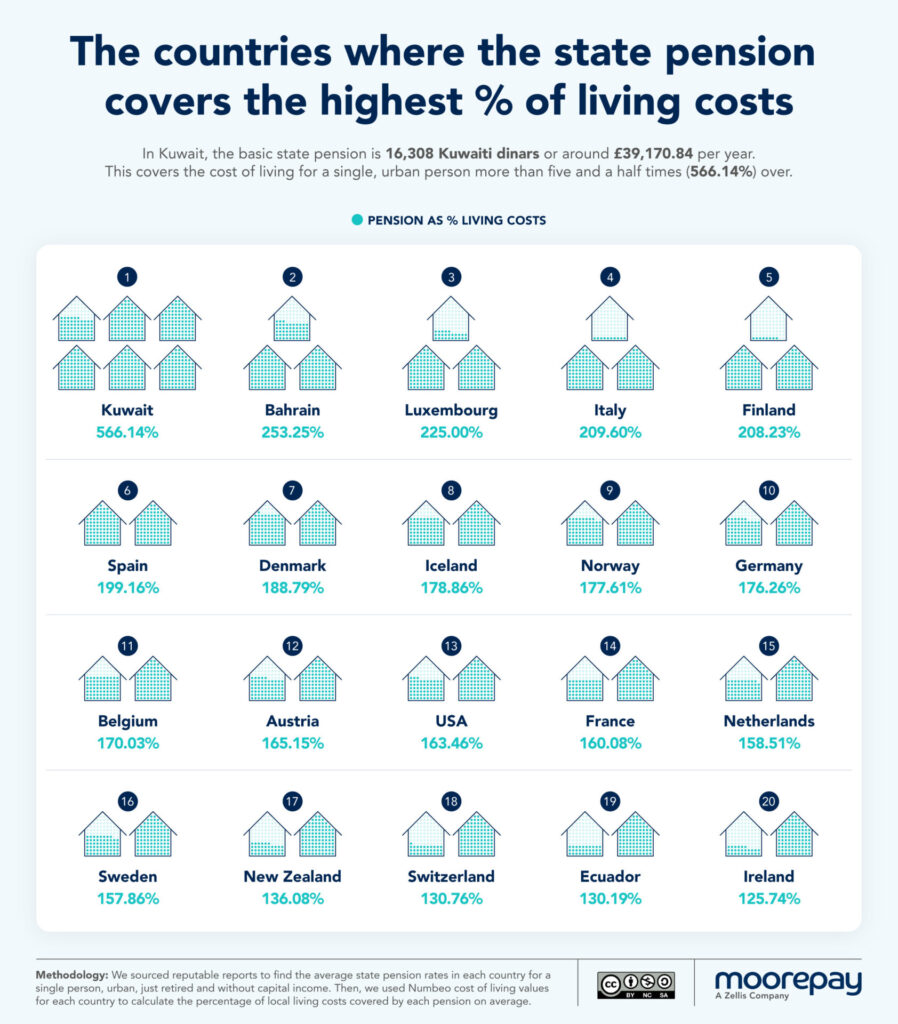

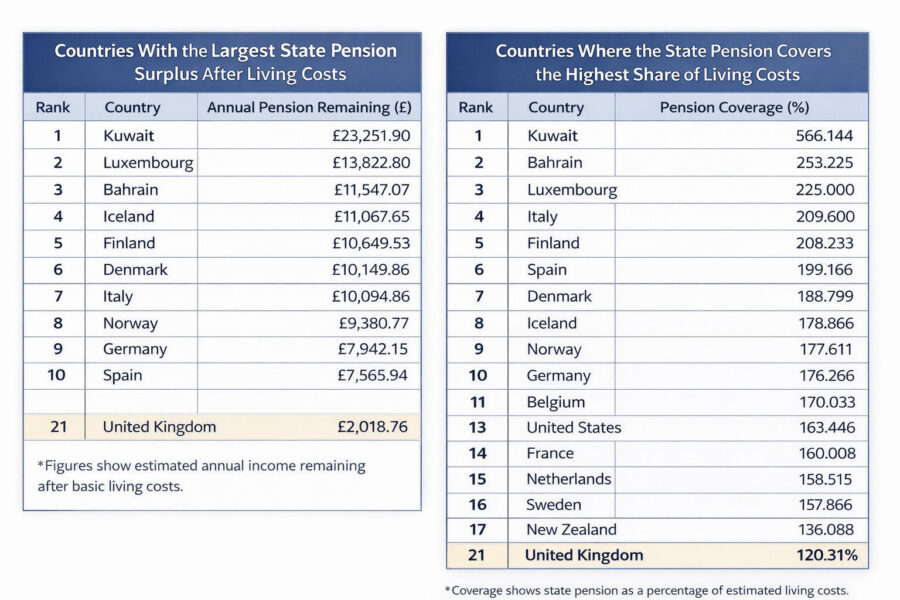

The analysis comes from a global study by HR and payroll software provider Moorepay, which compared state pension payments in 85 countries against local living costs. It found the UK ranks 21st globally, with the State Pension covering around 120 percent of basic living costs.

After essentials, UK retirees are left with an estimated £2,018 a year in disposable income. That compares with around £10,094 in Italy and £13,823 in Luxembourg, leaving pensioners in those countries with five to seven times more spending power than their UK counterparts.

Across much of the European Union, state pensions typically cover between 150 percent and 225 percent of living costs, placing the UK well behind many neighbouring countries. The study also ranked the UK 28th globally for real pension buying power.

Longer working lives become a necessity

The findings add weight to evidence that growing numbers of people are delaying retirement or returning to work after drawing their pension. For many, paid employment is becoming a key way to bridge the gap between state provision and the cost of everyday living, particularly as inflation has eroded spending power.

Employers are already seeing the impact, with older workers making up a rising share of the workforce in some sectors. Flexible working, phased retirement and part-time roles are increasingly used to retain experienced staff while accommodating changing health and caring needs.

Workplace pension provision also takes on greater significance in this context. Where state income falls short, occupational and private pensions are becoming more central to financial security, increasing scrutiny of employer contributions, auto-enrolment thresholds and long-term reward strategies.

Policy debate intensifies ahead of April increase

The research lands amid renewed debate over the sustainability of the triple lock and proposals to raise the state pension age further. While the upcoming April increase will lift payments, the international comparisons suggest it may do little to close the wider gap in living standards between UK retirees and those elsewhere in Europe.

As a result, questions are growing about how long people can realistically be expected to work and what support employers and government need to provide to ensure longer working lives are healthy, productive and genuinely sustainable.

William Furney is a Managing Editor at Black and White Trading Ltd based in Kingston upon Hull, UK. He is a prolific author and contributor at Workplace Wellbeing Professional, with over 127 published posts covering HR, employee engagement, and workplace wellbeing topics. His writing focuses on contemporary employment issues including pension schemes, employee health, financial struggles affecting workers, and broader workplace trends.

- William Furney

- William Furney

- William Furney

- William Furney